Global markets are grappling with a dual-threat of surging energy prices and a hawkish pivot from the Federal Reserve as Brent crude breaches $120 amid escalating US-Iran tensions. While Big Tech earnings show a stark divergence between winners like Alphabet and losers like Meta, the overarching narrative is the return of “elevated” inflation and a collapsing bond market.

1. The Primer

The macro landscape has shifted violently overnight as the “transitory” ghost returns to haunt the Fed, with energy prices surging on reports of potential US strikes against Iranian infrastructure. Traders are recalibrating for a “higher for longer” reality as the 10Y yield pierces 4.40%, threatening to destabilize a semiconductor-heavy equity market.

2. The Macro Field

The Federal Reserve has officially abandoned its cautious optimism, upgrading its characterization of inflation from “somewhat elevated” to “elevated,” with PCE expectations now pegged at 3.5% for March 2026. This hawkish stance was underscored by a fractured FOMC, where four members dissented against the rate pause—the highest level of internal disagreement since 1992. Across the Atlantic, the Bank of England maintained rates at 3.75% in an 8-1 vote, with Governor Bailey admitting that monetary policy is largely powerless against the global energy shock currently driving Brent crude toward historic highs.

3. The Intraday Edge

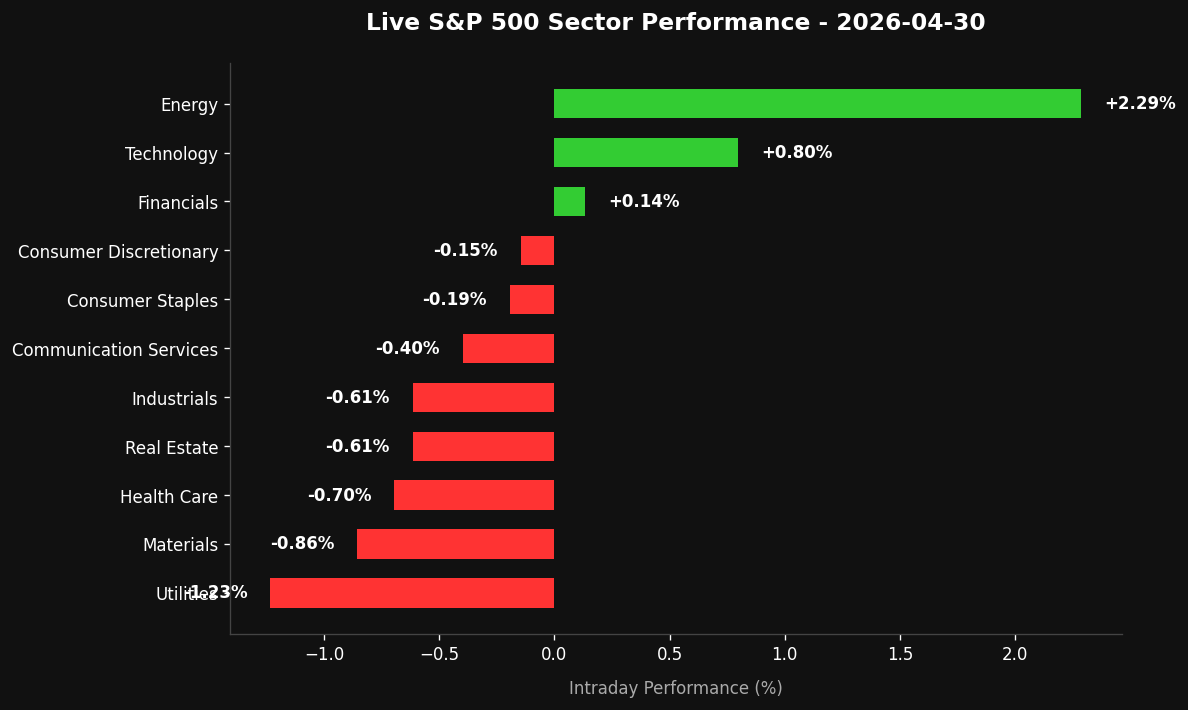

Sector focus must remain squarely on Energy ($XLE) and Crude Oil futures, as the geopolitical risk premium is being aggressively priced back in; Brent breaking $120 and WTI clearing $110 suggests a momentum squeeze is underway. In the equity space, we are seeing a brutal “perfection or death” filter in earnings: Alphabet ($GOOGL) is surging +5% on a clean beat, while Meta ($META) and Amazon ($AMZN) are being sold off -7% and -6% respectively despite strong numbers, indicating a liquidity drain from high-duration assets. Watch the 4.40% level on the 10Y Yield with extreme prejudice; if this level holds as support, expect further compression in the semiconductor industry, which now accounts for a record 41.9% of the IT sector’s total market cap and remains highly sensitive to discount rate volatility.

4. The Execution (Psychology)

In an environment where the Fed admits inflation is back and geopolitical headlines can move oil $5 in minutes, your primary job is risk mitigation, not hero calls. The “dissenter” count at the Fed is a flashing red light of policy uncertainty; when the pilots are arguing in the cockpit, the disciplined trader tightens their stops and reduces position sizing. Avoid the “dip-buying” reflex in high-beta tech until the bond market finds a floor, as the 10Y yield at 4.40% acts as a gravity well that will continue to pull down overextended valuations.

5. Bottom Line

The “Inflation is Back” narrative is the new dominant regime; prioritize Long Energy and defensive positioning while treating the 4.40% 10Y yield as the ultimate line in the sand for risk-off sentiment.

Leave a Reply