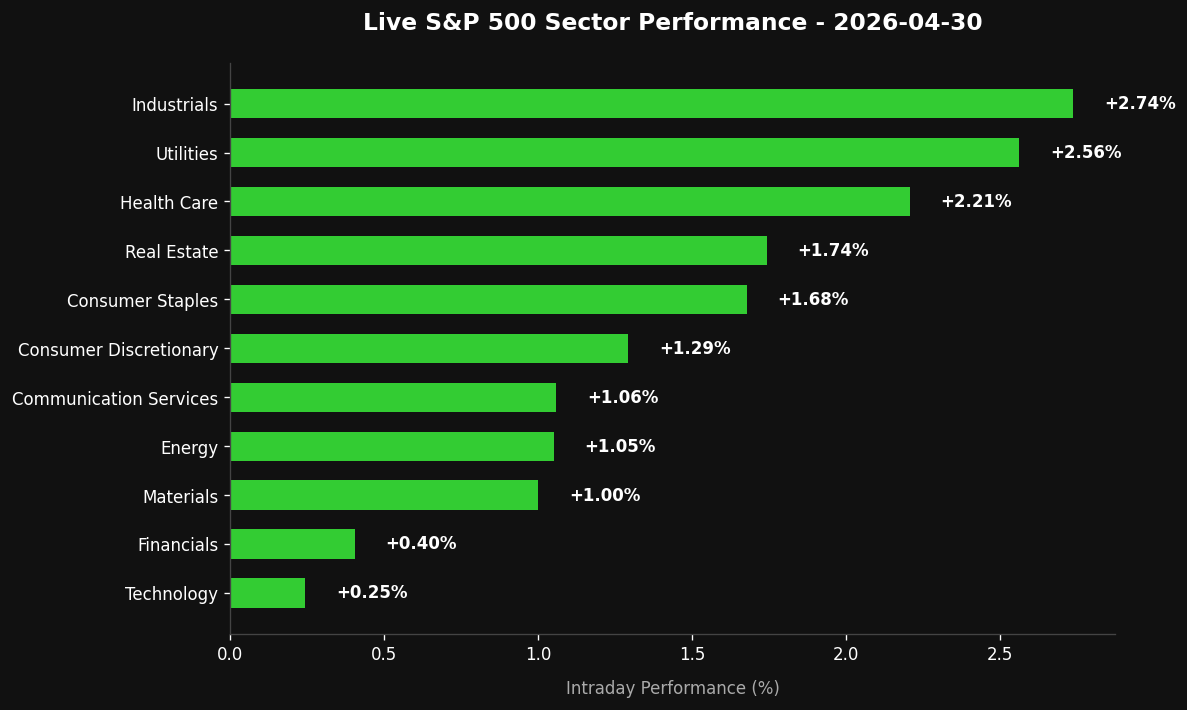

The Primer: Markets digested a “meet-the-mark” PCE print that confirmed sticky inflation without triggering a fresh panic, while Apple’s massive $100B buyback authorization acted as a primary stabilizer against regional revenue misses. Geopolitical friction remains the overnight wildcard as the Strait of Hormuz becomes a focal point of rhetoric between Tehran and Washington.

1. The Macro Field

The March PCE Price Index arrived exactly in line with consensus at 3.5% Y/Y, with the Core reading holding at 3.2%. While these figures confirm that the “last mile” of inflation remains stubborn, the lack of an upside surprise provided a relief valve for Treasury yields. Meanwhile, the currency markets faced a jolt as the Nikkei confirmed a Japanese Yen-buying intervention, signaling that the BoJ is no longer willing to tolerate speculative devaluations. In the Eurozone, Christine Lagarde signaled a steady hand, noting a lack of second-round effects, which keeps the ECB on a divergent path from the Fed’s “higher for longer” stance.

2. The Intraday Edge

The session’s narrative was dominated by Apple’s ($AAPL) Q2 earnings, which presented a classic “good news, bad news” setup. While the $111.18B revenue beat and the record-breaking $100B share buyback provided an immediate institutional floor, the miss in Americas and Europe revenue suggests a cooling in core consumer demand. Traders should watch the $AAPL supply constraint narrative closely, as Tim Cook’s admission regarding advanced node chips highlights ongoing friction in the semiconductor tailwind. In the crypto space, we observed a massive liquidity injection with $1.25 billion in USDT and USDC minted at treasuries; this “dry powder” accumulation often precedes a volatility expansion, even as BTC flows to exchanges like Robinhood suggest retail distribution is meeting institutional bids.

3. The Intraday Edge

Institutional sentiment is currently bifurcated between the “Buyback Shield” in Big Tech and the “Geopolitical Risk” in Energy. Trump’s commentary regarding a potential deal with Iran, contrasted with Iran’s threats to the Strait of Hormuz, has created a high-noise environment for Crude Oil. For the next session, the edge lies in ignoring the political rhetoric and focusing on the $USDC/USDT minting signals—liquidity is being staged for a move. If the $AAPL buyback bid holds the QQQ above key support levels, expect a rotation back into high-beta names, but keep a defensive posture in FX as the Yen intervention creates unpredictable cross-currency ripples.

4. The Execution (Psychology)

High-performance trading requires the ability to distinguish between “Signal” and “Noise.” Today’s session was flooded with noise—from Trump’s critiques of late-night television to speculative headlines about German Chancellors. Your mental model must prioritize the PCE data and the Apple buyback; these are the structural realities that move capital. Discipline today means not “revenge trading” the Yen volatility or chasing the Iran headlines. When the macro data hits the estimate exactly, the market often enters a “choppy” equilibrium; the elite move is to sit on hands until the post-earnings institutional rebalancing provides a clear directional trend.

5. Bottom Line

The inflation path is flat but firm, Apple’s buyback provides a tech safety net, and massive stablecoin inflows suggest a liquidity-driven move is brewing—stay patient and wait for the post-intervention dust to settle in the FX markets.

Leave a Reply