1. The Primer

Escalating geopolitical friction in the Middle East and a massive -9.1M barrel API crude draw have pushed energy markets to a knife-edge, while surging G7 bond yields force market participants to price in hawkish policy pivots ahead of the London open. As early European liquidity comes online, traders must navigate a complex backdrop of potential rate hikes from both the ECB and the Fed amid historic, top-heavy divergence in equity market breadth.

2. The Macro Field

While the scheduled Forex Factory economic calendar remains relatively light on top-tier data releases this morning, the real macro narrative is being driven by a global yield crisis and hawkish central bank posturing. G7 10+ year sovereign yields have surged to approximately 4.7%—their highest levels since 2004—as the market actively prices in the reality of a rate hike by incoming Fed Chair Kevin Warsh, alongside warnings from Fed’s Paulson that “super-elevated” inflation risks could trigger hikes if growth exceeds potential. Across the Atlantic, the ECB’s Kocher has explicitly tied monetary policy to geopolitical developments, warning of a potential June rate hike if the Iran conflict fails to show signs of de-escalation.

This hawkish backdrop is compounded by a massive -9.1M barrel draw in US API crude inventories and the US seizure of an Iran-linked tanker in the Indian Ocean, keeping Brent pinned near $111/bbl. With Citi forecasting Brent to hit $120 in the near term and presenting a bull case of $150, the energy complex is acting as a primary transmission mechanism for global inflation expectations, overriding standard equity market optimism and forcing sovereign debt yields to levels not seen since the Great Financial Crisis.

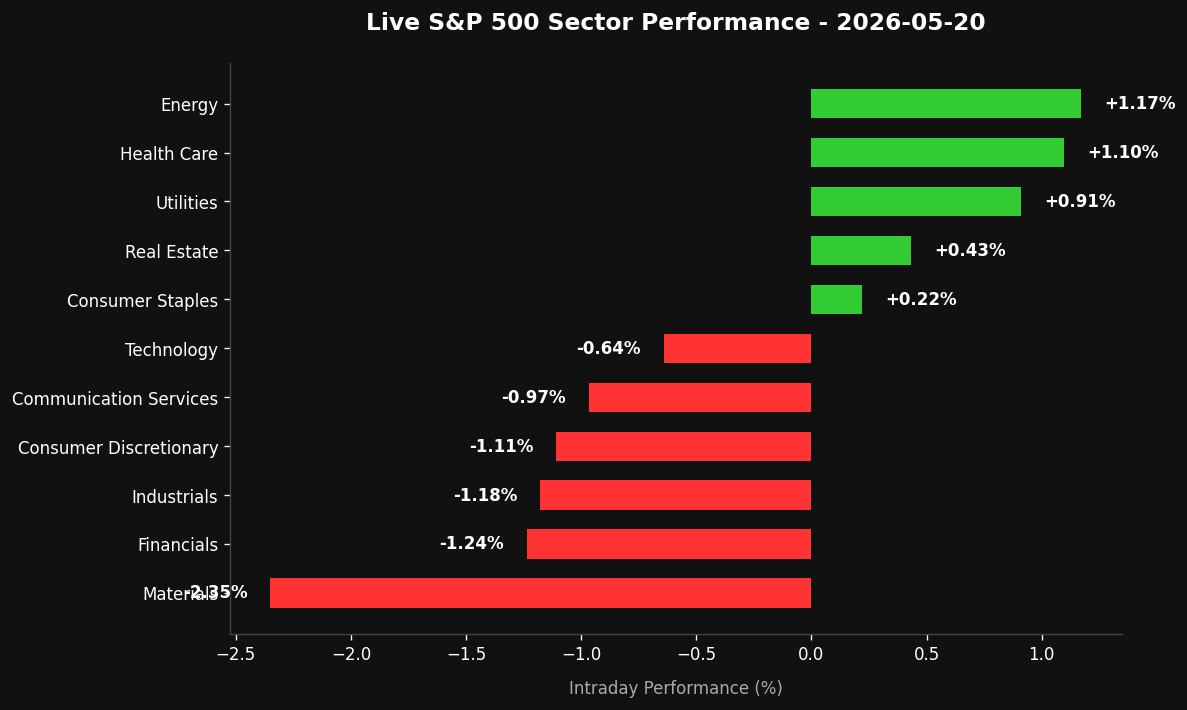

3. The Intraday Edge

Sector Focus: Crude Oil (WTI/Brent), Sovereign Debt (G7 Yields), and Mega-Cap Tech (following Meta’s announced 8,000 global job cuts and SpaceX’s IPO filing lead by Goldman Sachs).

The Setup: The energy complex is highly coiled. The US shadow fleet crackdown is intensifying with the seizure of the Skywave tanker, and US refineries are running at a record 12.7% jet fuel yield to meet wartime demand. We are looking for a breakout play on Brent Crude. If Brent holds above $111.00 during the London open, we anticipate a squeeze toward the $112.50 resistance level. Conversely, the equity space is showing structural fragility; the S&P 500’s historic divergence from overall market breadth (29 days of negative breadth on positive close days) suggests a top-heavy market vulnerable to yield-driven shocks. We are leaning short on equity index futures if US 10-year yields breach and hold above the critical 4.70% threshold.

Key Levels to Watch:

• Brent Crude: Pivot at $111.28; Resistance at $112.50 and $114.00; Support at $109.50.

• US 10Y Yield: Key psychological level at 4.70%; a break higher targets 4.85%, which will heavily pressure high-beta tech.

• EUR/USD: Watching the ECB rate hike rhetoric; support at 1.0800, resistance at 1.0880.

4. The Execution (Psychology)

In environments dominated by geopolitical headlines and structural yield shifts, the temptation to overtrade the “noise” is exceptionally high. High-performance execution requires you to apply the “Information Filter” mental model: distinguish between structural macro shifts (surging sovereign yields, physical oil draws) and transient political theater (headlines regarding potential negotiations). Do not chase the intraday spikes triggered by unverified social media reports or political posturing; instead, wait for price confirmation at key structural levels. Protect your capital by reducing position sizes to account for the elevated volatility regime, and accept that sitting on your hands during choppy, headline-driven ranges is an active, highly profitable decision.

5. Bottom Line

The London open is defined by a dangerous cocktail of rising yields and geopolitical risk; prioritize capital preservation by focusing exclusively on high-volume breakout levels in Brent and avoiding the choppy, low-breadth equity indices until US cash open clarity.

Leave a Reply