1. The Primer

Geopolitical escalation in the Middle East and a deepening sovereign debt selloff sent shockwaves through Wall Street, driving the 10-year Treasury yield to its highest level since February 2025 and triggering a heavy $1.07 billion sell-side Market-on-Close imbalance. As crude oil inventories post a massive 9.1-million-barrel draw amid reports of mining in the Strait of Hormuz, institutional desks are bracing for a stagflationary regime shift marked by rising global inflation forecasts and hawkish central bank pivots.

2. The Macro Field

While the formal Forex Factory calendar remained light on high-tier sovereign data releases today, the macro narrative was violently hijacked by geopolitical developments and sovereign debt repricing. The United Nations slashed its 2026 global economic growth forecast to 2.5% (down from 2.7%) while aggressively hiking its global inflation projection to 3.9%, citing severe energy disruptions stemming from the Middle East conflict. This stagflationary impulse was validated by the US API inventory report, which revealed a massive -9.1 million barrel crude draw (significantly deeper than the -3.4 million forecast), alongside a -5.8 million barrel gasoline draw. Simultaneously, US 30-year mortgage rates surged to 6.75% as the bond selloff intensified, pushing yields to multi-month highs and prompting warnings from Wolfe Research that rising yields—rather than equity drawdowns—will ultimately force the White House’s hand.

3. The Intraday Edge

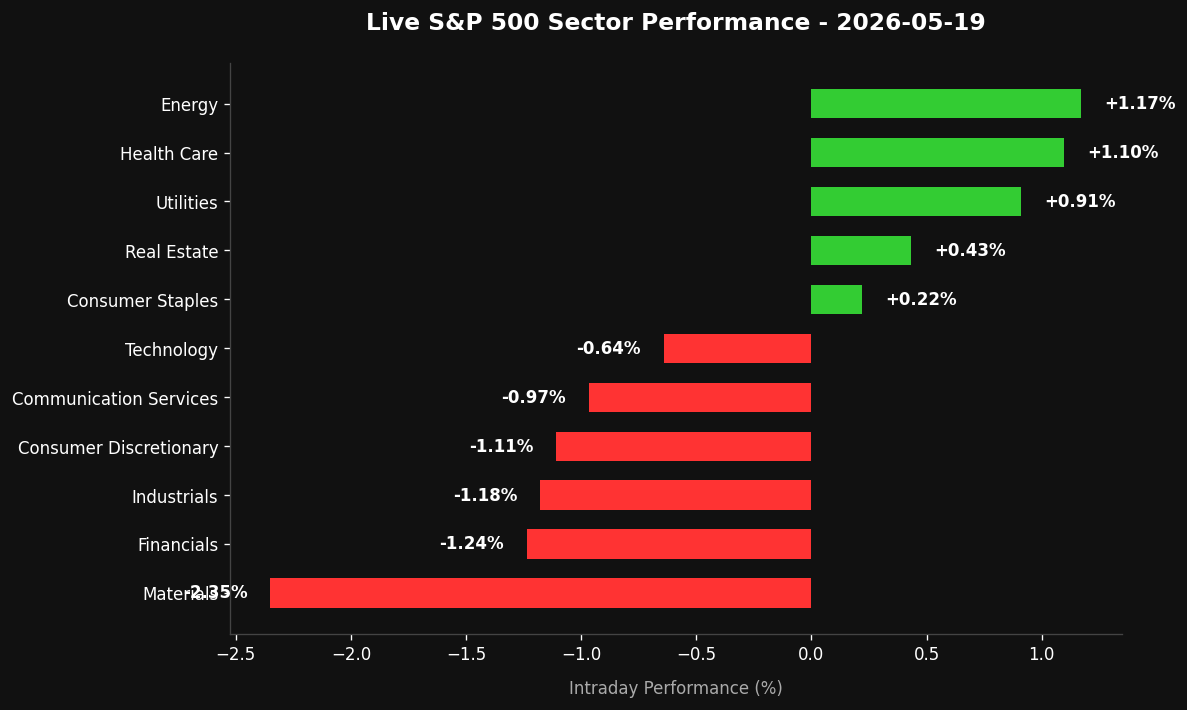

Institutional flow was decidedly defensive today, characterized by a massive $1.07 billion sell imbalance at the close for the S&P 500 and a $421 million sell-side tilt in the Nasdaq 100. Energy ($XLE) and defense sectors remain the primary tactical hideouts as Citi warns that Brent crude is fundamentally underpriced on tail risks, projecting a near-term target of $120/bbl and a bull case of $150/bbl if the Strait of Hormuz remains closed. On the corporate front, Meta Platforms ($META) faced antitrust headwinds after offering rivals limited WhatsApp access subject to messaging fees, while Lululemon ($LULU) saw talks with Wilson collapse, triggering immediate sell-side pressure. Key levels to monitor overnight include the recent swing lows on the S&P 500 as the index digests the hawkish ECB commentary from Kocher, who explicitly threatened a June rate hike if the Iran conflict does not de-escalate.

4. The Execution (Psychology)

In highly volatile, headline-driven regimes, the amateur tries to trade every geopolitical rumor, while the elite professional focuses strictly on position sizing and liquidity preservation. Today’s reports of strikes in Tehran and mining in the Strait of Hormuz are classic “known unknowns” that generate extreme noise and erratic price gaps. Your edge does not lie in predicting military outcomes or political maneuvers; it lies in managing your risk parameters so that no single headline can compromise your capital base. When the Market-on-Close imbalance prints a heavy sell-side bias and bond yields are ripping, the highest-performance action is often to reduce leverage, widen your stops, and let the market prove its structural bottom before deploying size.

5. Bottom Line

Protect your capital by avoiding over-leveraged overnight exposure in equities, and focus on the structural breakout in energy and yields as the market prices in a prolonged stagflationary shock.

Leave a Reply