1. The Primer

Wall Street staged a stunning 70-point intraday reversal to close the S&P 500 above 7,400, defying a scorching CPI print that sent inflation to a three-year high. While the Nasdaq initially buckled under the weight of a bond market meltdown, late-session institutional absorption suggests a “buy the bad news” regime is attempting to take root despite surging yields.

2. The Macro Field

The macro narrative shifted from “disinflation” to “re-acceleration” today as April CPI hit 3.8%, the highest level since May 2023, driven by a 29.2% surge in energy commodities. With oil breaching $102/barrel amid escalating Iran-Israel tensions and the 30-year yield crossing the psychological 5.00% threshold, the market has officially priced out rate cuts for 2024, with odds for a 2026 hike now climbing to 31%. This “inflationary shock” is being compounded by a record-breaking run in Copper, which hit $6.58 per pound, signaling that the cost of the AI-driven data center build-out is becoming a primary driver of global price pressures.

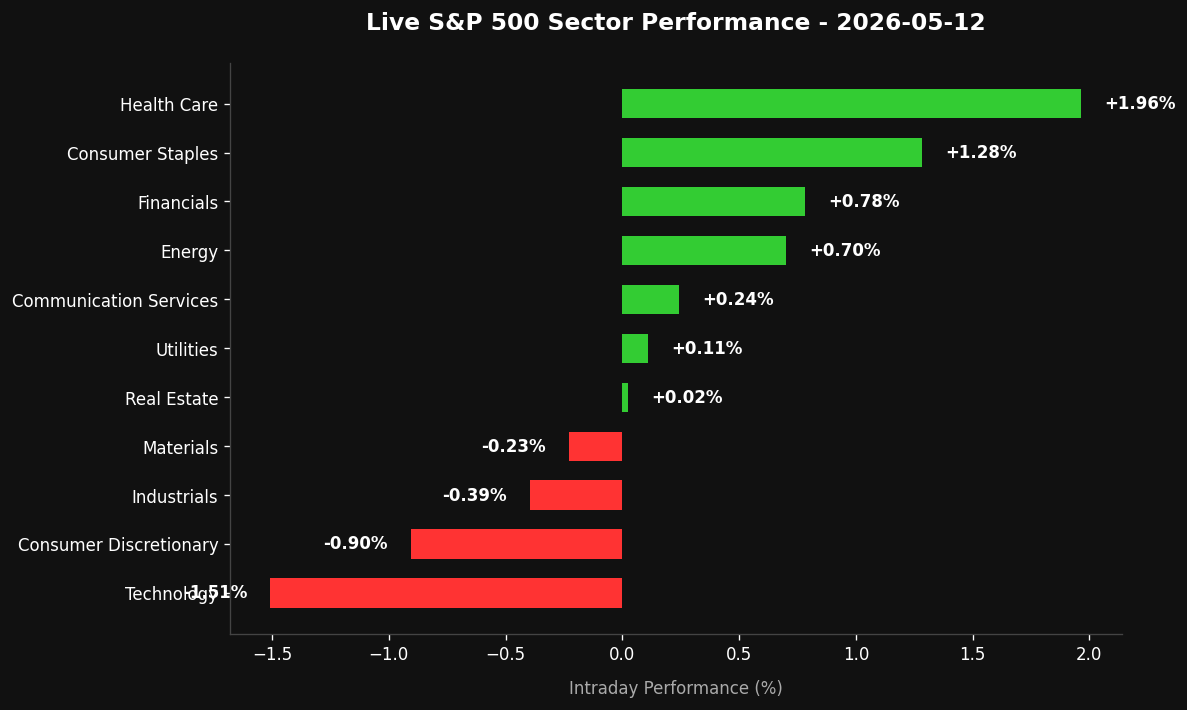

3. The Intraday Edge

Institutional flow today was characterized by extreme sector divergence and a “V-bottom” recovery at key structural levels. Despite the Nasdaq 100 falling over 2% in early trading, the S&P 500 found a massive bid at the 7,330-7,350 zone, eventually turning green as the Dow erased all CPI-induced losses. We are observing a dangerous narrowing of market breadth, with only 22% of stocks outperforming the index, while the Semiconductor Index ($SOX) now commands a record 23% of the total S&P 500 market cap. Watch the 4.50% level on the 10Y yield; institutional X sentiment suggests this is the “line in the sand” where equity valuations will face their most significant stress test since the 2023 lows.

4. The Execution (Psychology)

The mental model for today’s session is “Cognitive Dissonance Management.” High-performance traders must be able to hold two opposing truths: the macro data is objectively bearish (rising inflation, surging yields), yet the price action is resiliently bullish (70-point reversal). Discipline in this environment means ignoring the “logic” of the headline and respecting the “reality” of the tape; if the market refuses to go down on bad news, it is not ready to top. Avoid the trap of “revenge shorting” into a rising bid just because the CPI print was hot.

5. Bottom Line

The S&P 500 has reclaimed the 7,400 handle, but with the 30Y yield above 5% and oil at $102, the margin for error is razor-thin; stay long only while 7,380 holds on a closing basis.

Leave a Reply