1. The Primer

Global markets are navigating a volatile cocktail of record-high equity valuations driven by AI dominance and surging geopolitical tensions as the US-Iran ceasefire teeters on collapse. While the S&P 500 hits new peaks, the underlying breadth is dangerously thin, leaving the London open to grapple with $105 Brent crude and renewed UK political instability.

2. The Macro Field

The macro narrative is shifting from “higher for longer” to “much later for longer,” with Bank of America pushing rate cut expectations out to mid-2027 amid sticky inflation and a hawkish Fed trajectory. Geopolitical risk is the primary driver this morning; reports of secret UAE strikes on Iran and President Trump’s “life support” comments regarding the ceasefire have sent energy prices soaring. Meanwhile, UK traders must now price in domestic leadership uncertainty following Deputy PM Lammy’s calls for Prime Minister Starmer to set a resignation timetable, adding a layer of political friction to the Sterling as London liquidity enters the fray.

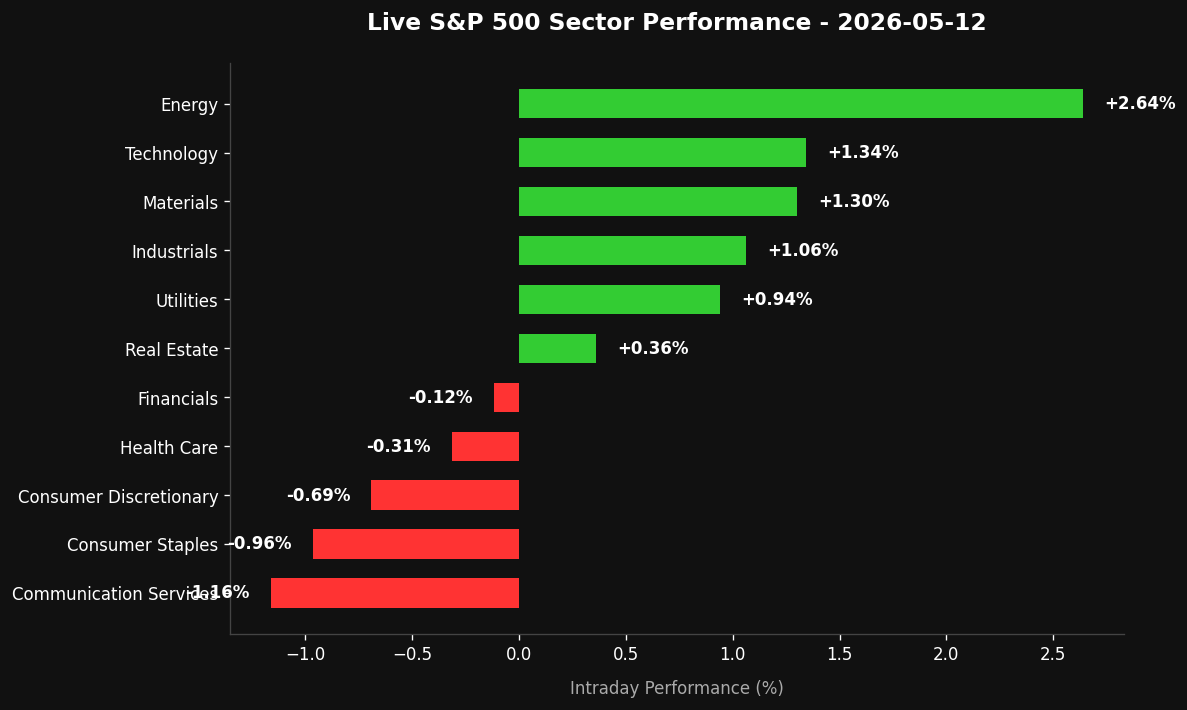

3. The Intraday Edge

Sector focus remains squarely on Energy and Safe Havens as Brent Crude tests the $105 handle and Silver surges 7% on war-premium pricing. In the UK, watch for the FTSE 100’s energy heavyweights—BP and Shell—to provide a potential cushion against Sterling weakness triggered by the Lammy/Starmer rift. Despite the S&P 500 posting record closes, the “internal” health of the market is deteriorating, with only 22% of stocks outperforming the index; this suggests a “top-heavy” environment where any cooling in the Semiconductor sector ($SOX) could lead to rapid deleveraging. Key levels to monitor: Brent Crude at $105.00, Gold/Silver resistance zones, and the 1.2450 pivot in GBP/USD.

4. The Execution (Psychology)

Beware the “All-Time High” Trap. When indices hit records while market breadth is at its lowest reading since 1996, the environment is fragile, not robust. High-performance discipline today requires resisting the urge to chase equity breakouts that lack broad participation. Instead, apply your mental capital to the “Real World” volatility in commodities where the narrative is backed by physical supply-chain risk and escalating geopolitical friction. If the London open presents a “gap and trap” scenario in UK equities due to political headlines, the professional move is to sit on hands until the volatility stabilizes.

5. Bottom Line

Long Energy and Silver on geopolitical tailwinds, but maintain defensive posture and tight stops on UK-sensitive assets as domestic political risk adds unpredictable friction to the session.

Leave a Reply